Market Outlook of This Week (12-April) - IT transforming into SaaS

- Normal Guy

- Apr 16

- 37 min read

Updated: 5 days ago

Disclaimer: This is not a buy or sell recommendation. I’m not a SEBI-registered investment advisor, and nothing shared here should be taken as financial advice. This content is purely for educational and informational purposes. I’m not affiliated with SEBI or any brokerage, nor am I trying to promote or sell anything. Always do your own research before making any investment decisions.

Market this Week

This week the whole market moved on one thing - the US-Iran ceasefire that came on Tuesday night, Apr 7. Before that, Nifty was bleeding for 6 weeks straight. After that, everything ripped. Oil crash is only on paper. Physical Brent cargoes are still trading $30 above futures because 13 million barrels a day of Middle East production is still shut-in and tankers are sitting at US ports. Qatar Ras Laffan LNG plant (20% of global LNG) also took damage - 17% capacity gone. So if Islamabad talks this weekend break, oil snaps back hard and the whole rally reverses. That’s the single biggest fragility.

On India macro, RBI held repo at 5.25% on Apr 8 with neutral stance, CPI projection 4.6%, GDP 6.9%, oil assumption 85 basically a wait and watch. 10Y yield fell from 7.13% to 6.9% - big 20bp move. US CPI on Friday printed hot at 3.3% YoY (highest since Apr 2024), but core was tame at 2.6% - so the spike is all energy, and Fed is essentially frozen with just 25% chance of a cut this year. Diesel export duty was hiked to ₹55.5/litre on Apr 11 - directly hits OMCs and airlines.

FPIs pulled ₹1.14 lakh crore from India in March - the biggest monthly outflow in Indian history, beating the Oct 2024 record. YTD outflow ₹1.27 lakh crore. Financial Services alone lost ₹31,831 cr of FPI money in just the first half of March. The ONLY sector FPIs bought was Capital Goods (+₹3,897 cr) - which is why L&T ripped 9.6% this week, its best week in 5 years.

So the rally you’re seeing is domestic-funded: DIIs + SIP flows of ₹30,000+ cr per month are the entire floor. FIIs only turned net buyer on Apr 10 - one day.

Sectorally, all 16 sectors were green - reason is oversold bounce breadth. VIX crashed 20% to 19.2. But the one sector that broke ranks was IT - Nifty IT -1.9% on Friday despite TCS posting clean Q4 numbers (profit +12% to ₹13,784 cr, record $12 billion TCV, ₹31 final dividend). TCS stock itself fell 2.5% because annual revenue disappointed. That last bit is genuinely weird and worth if yu Notice - when war doesn’t help gold, it means liquidity-driven selling is dominating fundamentals across assets. But Central Banks are going with Gold.

Let’s look at Strength & Weakness

NOTE: RRG scan and EMA 50 scan look similar, but they do very different jobs. RRG scan tells you where money is moving between sectors compared to Nifty 500. It shows direction and rotation, meaning which sector is starting to gain interest and which one is slowly losing it. It is about change and what may happen next. EMA 50 scan tells you how healthy a sector is right now by showing how many stocks inside that sector are already above their trend levels. It is about current condition, not future movement. In simple words, RRG shows the flow of money, while EMA 50 shows the present strength. One talks about direction, the other talks about health.

This is Below RRG chart :)

OUTLOOK

Again if you look at from At least September 2025 long term data, what you can understand from this is - sectoral tailwind sector will sooner or later lead. This is the foremost example. From September 2025, seeing this data (or you’ve seen in my article, okay), I feel metal will come again in a selective way, even healthcare also — but it will take time.

As of now, why are some sectors leading? Go look at their QoQ combined growth rate of that sector.

Why Pharma is leading, this Graph is Yur Answer :)

Well, Russia–Ukraine deal is close. US will find a way to deal with Iran, but it will not be easy - means Middle East will be unstable. US is also checking if the chain of command is working, or Iran has gone rogue. So as of now, anything can happen. Pak Hosting is now done deal after 15 hours of Talk :)

But I am still in favour of India, we are doing well. Volatility will come, but short term only.

MTF is declining, but not in consolidating phase. If things improve, the positiveness will increase rapidly

SECTOR & INDEX ROTATION

If you connect the dots with the RRG chart - Metal, Power, Capital Goods, Energy, Industry, Commodities, Platform business - all are doing good. You just have to correlate, okay.

In my view, these will stay for a while. This is a bear market, you have to understand this. And this will slowly change with the nudge of quarterly results and sectoral catalyst, that will matter.

You can also check this at the company level, because the category-wise division here is very niche and highly selective. This makes it easier to spot specific names. You can find the company names directly on StockScan and track them from there:

CORPORATE FILINGS

Must read the announcements that I have tick-marked 💯☑️. These are valuable if you use them wisely, so do go through them carefully. If you like what you see and want to read more, you can check them on Screener or anywhere else. These are strategic announcements from the last one week.

KEC Internationa - Awarded Rs 7.23 crore contract to HRS Aluglaze for supply of aluminium composite cladding sheets, part of larger order over Rs 26.94 crore. Company also secured new orders worth Rs 2,518 crores including its largest commercial real estate order and significant projects in transportation and transmission.

Motherson - Announced dissolution of indirect wholly owned subsidiary SMRC Automotive Interior Modules Croatia due to lack of business prospects and significant annual costs. Subsidiary’s turnover for FY 2024-25 was €256,362, negligible contribution. Also announced settlement of subcontracting dispute involving subsidiary SMR Hyosang Automotive Ltd with payment of KRW 360 million (INR 22.18 million)

Reliance - Anant Ambani launched Vantara University in Jamnagar, Gujarat, aimed at addressing global shortage in wildlife conservation and veterinary sciences. Also, India’s shipping ministry granted one-time exemption for four Iranian oil tankers to berth at Sikka port due to Strait of Hormuz closure emergency. Bombay High Court ruled in favour of RIL, directing MMRDA to refund Rs 646 crore penalty deposited for alleged construction delays, calling penalty arbitrary. Jio-bp capped diesel sales at 50 litres per customer daily amid supply crunch. Reliance capped fuel purchases at $11 per visit at retail outlets amid Middle East crisis shortages, first company to implement rationing beyond price hikes. Sunil Singhania-backed Abakkus Flexi Cap Fund raised stake in RIL in March. Helios Flexi Cap Fund increased stake in RIL (5.24% of AUM). Reliance also participated in pre-bid talks with government for $780-mn rare earth magnet manufacturing scheme. Reliance has not clarified potential investment in new US oil refinery. 💯☑️

Dixon - Part of India Cellular and Electronics Association advocating for new PLI 2.0 scheme to sustain and grow smartphone manufacturing in India, India eyes 35% global mobile output, $130 billion production.

HUDCO - Signed two MoUs with NBCC (India) Limited for redevelopment of 18,830 sqmt plot in New Delhi and asset monetization for NBCC’s self-sustainable projects.

Mazagon Dock (MAZDOCK) - Acquired 51% stake in Colombo Dockyard for Rs 249.5 crore, marking first international acquisition and strategic expansion into regional market, aligning with India’s long-term maritime strategy.

Maruti Suzuki - Plans to launch four new EVs by 2031, aims to become leading BEV market player. Recently delivered 108 units of e-VITARA in a single day in Hyderabad and has set up over 2,000 exclusive charging points across India. Also facing supply chain issues due to Iran war, affecting delivery timelines particularly for high-demand models.

Enviro Infra Engineers (EIEL) - Received Letter of Empanelments for two projects in Maharashtra totaling ₹972.190 Crores, involving STPs and sewer network development under Swachh Bharat Mission, 24-month completion timeline. 💯☑️

Adani Enterprises - Adani Airport City Limited (step-down wholly owned subsidiary) incorporated four new subsidiaries - Adani Mangaluru Airport City, Adani Jaipur Airport City, Adani Lucknow Airport City, and Adani TRV Airport City, each with paid-up share capital of ₹10,00,000. Also, Vedanta alleged Jaiprakash bid process was ‘tailor-made’ for Adani despite higher offer; lenders preferred Adani’s plan due to higher upfront cash offer. Gautam Adani moved to dismiss US SEC fraud case, US court granted hearing for preliminary dismissal plea, group stocks surged. Supreme Court refused to stay Adani’s Rs 14,500 cr JAL resolution plan in blow to Vedanta.

HDFC Bank - Nomination and Remuneration Committee (NRC) set to meet April 17 to discuss new chairman appointment, Jagdishan reappointment not on agenda yet. RBI said no systemic risk from sudden exit of former chairman Atanu Chakraborty. RBI Governor Sanjay Malhotra revealed plan for revision of bank board guidelines following HDFC Bank issues. Sebi chairperson highlighted heightened scrutiny of corporate governance after Chakraborty exit citing incongruity in values. Bank may leave Bhavesh Zaveri board seat vacant after his April 12 retirement. Also among empanelled banks for YEIDA residential plot scheme financing.

M&M (Mahindra & Mahindra) - Approved acquisition of 26% stake in Neon Hybren Private Limited for Rs. 11.17 crores to support development of 30 MW solar power project in Punjab. Also facing supply chain disruptions due to Iran war.

Great Eastern Shipping (GESHIP) - LPG tanker Jag Vikram became first India-flagged vessel to transit Strait of Hormuz after US-Iran ceasefire, carrying 20,000 tonnes of LPG, deadweight capacity exceeding 26,000 tonnes. Contracted to sell 2003 built Medium Range Tanker Jag Pankhi (46,273 dwt) to unaffiliated third party, delivery Q1 FY27, fleet currently 40 vessels. Also contracted to sell 2007 built Medium Range Tanker ‘Jag Prakash’ (47,848 dwt) to unaffiliated third party, delivery Q1 FY27. 💯☑️

NTPC - Subsidiary THDC India declared COD for 4th Unit (250 MW) of Tehri PSP effective April 12, 2026, taking total installed capacity to 89,378 MW. Announced uprating of Dadri Thermal Power Station Units 5 and 6 from 490 MW to 500 MW each, total installed capacity now 89,128 MW. Signed Non-Binding MoU with Électricité de France (EDF) to explore nuclear power project cooperation in India.

Zaggle - Signed two-year agreement with Generali Central Insurance Company to provide Zaggle Zoyer Platform, part of ongoing business operations.

Medplus Health Services - Subsidiary Optival Health Solutions received five-day drug license suspension in Odisha, potential revenue loss Rs 3.80 lacs. Also received two-day Drug License suspension in Telangana, potential revenue loss Rs 0.28 lacs.

NHPC - Firming up investment proposal for 3,000 MW Etalin hydropower project in Arunachal Pradesh with Rs 30,000 crore investment. CCEA approved investment of ₹26,069.50 Crore for 1720 MW Kamala Hydro Electric Project in Arunachal Pradesh, expected to generate 6870 MUs annually, 96-month completion.

Paytm - Announced incorporation of wholly owned step down subsidiary PT PAYTM INDONESIA TEKNOLOGI in Indonesia, subscribed to 15,00,000 equity shares for Indonesian Rupiah 15 billion (INR 8.15 Crores).

Dabur - Imposed penalty of INR 4,00,000 by Addl. District Magistrate Almora for labelling contraventions under Food Safety and Standards Act, plans to appeal. Also returning to full capacity at local plants as export activities resume following Iran ceasefire.

Bharti Airtel - Airtel deployed over 4,300 new 5G sites across UP East in last 12 months covering 48 districts, 34 million people.

Tata Motors - Commenced deliveries of heavy-duty electric Prima E.55S trucks to BillionE Mobility, secured order for 250 additional electric prime movers. UK awarded $510 million to Tata’s Agratas for Somerset EV battery gigafactory (40 GWh capacity). Focusing on global expansion post demerger, aligning PV business with JLR, Iveco deal to boost CV footprint. Facing supply chain issues from Iran war with delays and tightening inventory. Tata Intra EV pickup launched at Rs 11.95 lakh, 211 km range, 1,750 kg payload, fast charging, 6-year/2 lakh km battery warranty. TPG led $1 billion investment in Tata Motors’ EV business. 💯☑️

Carborundum Universal - Signed Power Purchase Agreement with Putrim Renewables Private Limited for 18 MWp solar power, will acquire 29.58% equity in PRPL for Rs. 6.48 crores.

Suzlon Energy - Secured 100 MW wind energy order from GAIL, order book at 6 GW.

Syrma SGS Technology - Announced name change for joint venture company Syrma Strategic Electronics Private Limited per Joint Venture Agreement with SH Electronic Co. Limited. 💯☑️

Torrent Pharmaceuticals - USFDA inspected Bileshwarpura (Oncology) facility April 6-10, 2026, concluded with zero observations. Also emerged as largest local player in semaglutide market in India with 8% market share after Novo Nordisk patent expiry. 💯☑️

Apollo Hospitals - Received NCLT certified order on composite scheme of arrangement involving Apollo Healthco, Keimed Private Limited, and Apollo Healthtech.

Garware Hi-Tech Films (GRWRHITECH) - Introduced new product line including Graphic Films for branding, Cloaking Films for privacy, and PDLC Smart Films for dynamic spaces. 💯☑️

Thomas Cook - Inaugurated new franchise outlet in Guwahati, total three locations in Assam.

Sun Pharmaceutical - Clarified speculative news article regarding 4% stock drop due to alleged $12 billion Organon deal, stated information speculative and does not require disclosure. Preparing binding offer of $12 billion for Organon Co, most ambitious overseas acquisition after completing due diligence with global banks financing. 💯☑️

TCS - Reported modest margin increase due to currency movements and operational efficiencies, investing in AI and cybersecurity, $1 billion earmarked for capability building. Acquired 20-acre land parcel in New Town Kolkata for Rs 94 crore via 99-year lease. Renewed strategic partnership with Marks and Spencer, multi-year engagement focusing on AI and modern technologies. Announced annual salary hike across all grades effective April 1, 2026. Headcount dropped over 23,000 in FY26 amid layoffs, ended at 584,519. Reversed two-quarter headcount slide adding 2,356 employees in Q4FY26, restructuring expenses rose to Rs 1,388 crore, attrition 13.7%. Made AI-led multicloud Salesforce consulting firm acquisition expected to contribute 0.4% to Q4 FY26 revenue. Experienced unprecedented senior talent exodus with at least 300 of 1,800 senior executives leaving in past eight months (16% churn). TPG partnered with TCS for AI-ready data centers JV with Rs 8,820 crore investment. 💯☑️

IDBI Bank - Government initiated fresh valuation for sale of 60.72% stake, bidding decision expected after valuation (1 month). Kotak Mahindra Bank among short-listed bidders. Government may seek fresh bids as current bids (Rs 40,000-45,000 crore range) are below expected valuation and minimum reserve price.

Coal India - Absorbing increased operational costs including 44% rise in ammonium nitrate prices and 54% increase in industrial diesel prices to shield Indian coal users, reducing coal reserve prices in auctions.

Zydus Lifesciences - Among drugmakers that launched generic semaglutide in India. Received final USFDA approval for Dapagliflozin Tablets 5mg and 10mg for Type 2 diabetes, granted 180 days shared generic exclusivity, US annual sales USD 10.2 billion. Received favorable GST order, dropped demand of Rs. 41.77 million for FY 2019-20. 💯☑️

Power Mech Projects - Received ₹296.44 Crores order for operations and maintenance of Mumbai Monorail covering 19.54 km corridor with 17 stations over five years.

RailTel - Secured Rs 23.18 crore order from Goa Building and Other Construction Workers Welfare Board to develop online portal by June 8, 2026.

Park Medi World (PARKHOSPS) - Launched new multi-super specialty hospital in Panchkula, 850 bed capacity across key specialties, enhancing healthcare access in Tricity region. 💯☑️

Saatvik Green Energy (SAATVIKGL) - Subsidiary Saatvik Solar Industries secured Rs 108.75 crore order for solar PV modules by September 2026, received four different orders totaling Rs 723.77 crore in March 2026.

SBI - quared up net open positions of $5 billion in foreign exchange ahead of regulatory deadline.

Blue Star - Preparing for increased demand linked to Middle East reconstruction. Rolling out 13% price hike after already raising prices 8% in March due to rising material costs.

Hindustan Unilever - Focusing on reclaiming market share lost to rivals, plans D2C acquisitions, completed full ownership of Oziva and acquired majority stake in Minimalist, divested from Wellbeing Nutrition.

Prestige Estates - Announced joint venture with ABIL Group to develop 6-acre Versova Mumbai land parcel, 1.7 million sq ft potential, GDV over ₹9,000 crores. Acquired 50% partnership interest in Aaramnagar Realty LLP for Rs. 180 crores for Versova Mumbai real estate development.

GNFC (Gujarat Narmada Valley) - Stepping in to assist with logistics as pharma-grade methanol supply remains concern. Government in discussions with GNFC to enhance methanol supply.

VA Tech Wabag - Executed Shareholders Agreement with PEAK Sustainability Venture Fund I and Ghaziabad Bioenergy for Compressed Bio-Gas project, Wabag holds 5,100 equity shares, PEAK holds 4,900 shares. 💯☑️

Zomato - Surrendered payment aggregator and wallet licence, focusing on core food delivery and quick commerce.

Refex Industries - Received order valued INR 70.2 Crore for Bulk Industrial Commodity supply from Navratna PSU in steel sector, two-month execution. 💯☑️

Thermax - Completed acquisition of 51% stake in Exactspace Technologies Private Limited, making it subsidiary following February 27, 2026 agreement.

Sandur Manganese (SANDUMA) - Executed Forest Lease Agreement for 2.4314 hectares forest land in Karnataka for Downhill Conveyor Pipe System following MoEFCC approval. 💯☑️

Granules - Increasing oversight at manufacturing facilities and digitizing documents in response to US FDA warning regarding record-keeping and contamination control violations at largest plant, implementing automation and tighter controls.

Eicher Motors - Launched Flying Flea C6 electric motorcycle priced at ₹2.79 Lakh, bookings from April 10, 202, top speed 115 km/h, lightweight design.

HPCL (Hindustan Petroleum) - HPCL-Rajasthan refinery (9-MMTPA JV with Rajasthan Government) to be inaugurated by PM Modi on April 21, costs Rs 80,000 crore, to produce BS-VI fuels and key petrochemicals.

GAIL India - Plans to borrow 50-60 billion rupees in fiscal 2027 to fund expansion, Dabhol LNG import terminal operating below 5 mtpa capacity. Signed long-term charter party agreement with Alpha Gas for LNG carrier ‘Energy Fidelity’ (174,000 cubic meters capacity) supporting Maritime Amrit Kaal Vision 2047.

LTIMindtree - Launched Universal AI program from MIT Open Learning for employees in collaboration with upGrad Enterprise, MIT completion certificates to be awarded.

Pricol - Denied claims of acquiring 100% stake in German automotive components firm, labeling information incorrect and misleading.

Alkem - Among companies that launched generic semaglutide in India post patent loss. Launched A to Z Daily multivitamin supplement with 26 essential vitamins, minerals, botanicals, FSSAI approved.

Dr Reddy’s - Among first companies to roll out generic semaglutide in India. Entered agreement to sell entire shareholding in wholly owned subsidiary Svaas Wellness Limited for INR 2.23 Cr; Svaas contributed Rs. 28.5 Crore to FY 2025 turnover (0.09%).

Glenmark - Among drugmakers that launched generic semaglutide versions in India. Received final USFDA approval for Progesterone Vaginal Inserts 100 mg bioequivalent to Ferring Pharmaceuticals Endometrin, US market $59.2 million annual sales as of February 2026.

Datamatics - Launched TruAI Underwriting, Agentic AI-based solution for insurance underwriting, reduces TAT by up to 70%, lowers costs by 50%, improves accuracy by 25%. 💯☑️

HFCL - Subsidiary HTL Limited secured ₹1,366 crore orders for optical fiber cables from Tier-1 customer by December 2026; entered five-year supply agreement with global corporation valued ₹10,159 crore; announced ₹175 crore investment for acquisitions via subsidiary, order book increased to ₹11,125 crore as of December 31, 2025. 💯☑️

Hyundai - Launched Creta Summer Edition variants with added tech and safety features, prices Rs 12.05-17.88 lakh, existing powertrain line-up maintained. Announced car price increase up to 1% across portfolio effective May 2026 due to rising input costs.

Dilip Buildcon (DBL) - Via JV DBL-RBL declared L-1 bidder for Rs. 268 Crore EPC project of Ged Barrage across Sabarmati River, 24-month completion.

Persistent Systems - Launched Merchant Risk Management Solution using Databricks AI, reduces chargeback losses 20-40%, improves detection accuracy 30-60%, lowers manual review efforts 50-70%. 💯☑️

Escorts Kubota - Disclosed intention to launch new tractor series by Powertrac shortly. Also announced price increase for Kubota brand tractors effective April 15, 2026, varying across models and regions.

Adani Green Energy - Subsidiary AGEL UAE signed JV Agreement with Minerva Holding RSC Ltd to develop renewable energy projects in India, AGEL UAE to invest up to 20% in JVCo.

Apollo Micro Systems (APOLLO) - Successfully completed blast trials for Diver Carried Limpet Mines, only Indian company to develop this product for Indian Navy, key player in underwater electronic warfare. 💯☑️

Castrol India - Upgraded Castrol Activ and Castrol GTX to full synthetic formulations; new offerings include Activ 10W-30 and 5W-30, GTX 5W-30 and 0W-20, available across 150,000 retail outlets.

Tata Power - Partnered with Databricks for AI and Data Transformation to build future-ready data and AI platform enhancing operational efficiency and energy transition.

RateGain - Strategic partnership with Hotelogix enabling direct GDS connectivity via UNO Platform, reaching 600,000+ travel agents and corporate programs. 💯☑️

Allied Blenders and Distillers (ABDL) - Launched ZOYA PINK Mix Berries Gin priced at INR 2,500, blend of strawberry, cranberry, blackberry, raspberry; initial availability in Maharashtra.

Anant Raj - Entered Supplementary Agreement with Destination Properties for residential project collaboration in Gurugram Haryana on 5.0875 acres; Destination Properties entitled to 17.69% of total project revenue.

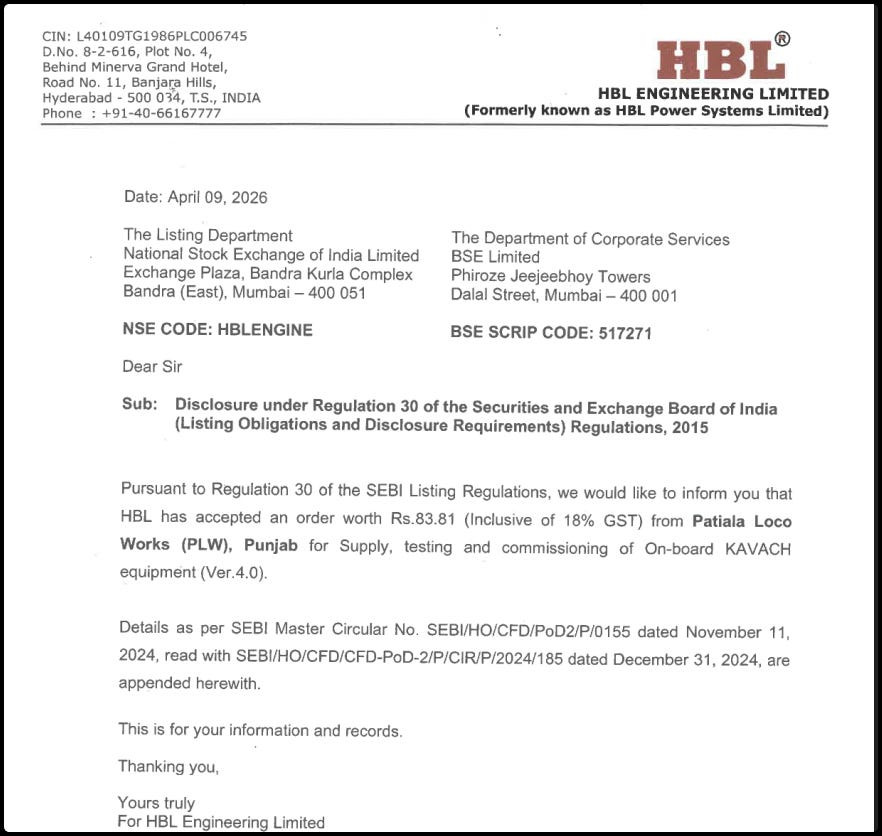

HBL Engineering (HBLPOWER) - Accepted Rs. 83.81 Crores order (incl. 18% GST) from Patiala Loco Works for supply, testing, commissioning of On-board KAVACH equipment (Ver.4.0) by April 15, 2027. 💯☑️

Premier Energies (PREMIERENE) - Secured ₹2,577 crore orders for 1,600 MW solar cells and modules in Q4 FY 2026, execution planned FY 2027 and 2028.

Vedanta - Ongoing demerger into five entities (aluminium, zinc, oil/gas, steel, power) emerged as key lender concern in JAL race. Likely to participate in pre-bid meet for Rs 7,280-crore rare earth magnet scheme.

Sri Lotus Developers (LOTUSDEV) - Launched first brand campaign ‘Luxury Coastline Collection’ featuring 11 projects across coastal Mumbai locations, expanding beyond Juhu and Andheri West.

Nava - Formerly Kluisz, raised $21.7 million Series A led by Greenoaks Capital to develop AI neocloud platform, shifting from private cloud to GPU-based infrastructure. 💯☑️

Tata Communications - Among nine companies that cleared technical stage in IndiaAI Mission GPU tender, concerned about rising costs and short contract cycles affecting AI infrastructure investment.

Zee Entertainment (ZEEL) - Preparing to launch sports channels, approached by FIFA regarding media rights indicating potential interest in expanding sports broadcasting.

Lupin - Received USFDA approval for Dapagliflozin and Metformin Hydrochloride Extended-Release Tablets bioequivalent to Xigduo XR. Completed acquisition of VISUfarma B.V. enhancing specialty care ophthalmology portfolio. Received USFDA approval for Dapagliflozin Tablets 5 mg and 10 mg bioequivalent to Farxiga. 💯☑️

Bank of Baroda - Launched AI-powered multilingual platform ‘bob SAMVAD’ for branch customer service in 22 Indian languages. Majority owner of IndiaFirst Life (64.98% stake) contributing significantly to new business premiums. Empanelled for YEIDA residential plot scheme financing.

Oil India (OIL) - Bangladesh formally requested increase in petroleum product exports from Numaligarh Refinery via India-Bangladesh Friendship Pipeline (currently 100,000 tonnes diesel annually).

Sansera Engineering - Appointed Mr. Rahul Kale as CEO-Automotive effective April 8, 2026, previously COO, with 20+ years experience at Gestamp and GKN Group. 💯☑️

Coforge - Introduced AI Mod Squads, subscription-based model combining AI agents with specialized engineers, showing 70% reduction in cycle time for banking loan origination. Announced AI-native firm deal expected to generate $2.5 billion revenue by FY27. Promoted Sunil Fernandes to COO, previously EVP - Global Delivery Head, overseeing global delivery and key operations to accelerate AI-native practices. 💯☑️

Bajaj Finserv - Led funding round of ₹80 crore for NowPurchase, AI-powered B2B metal procurement platform.

BEML - Signed MoU with Delhi Metro Rail Corporation to jointly bid for metro projects in West Asia, enhancing BEML’s rail and metro presence.

KFin Technologies - Approved amendments to Code of Practices and Procedures for Fair Disclosure of UPSI to align with PIT Regulations.

Redtape - Acquired international sports footwear brand SPRANDI for India, Nepal, Bhutan, Sri Lanka; launching soon through online and retail channels.

Bosch - Board approved acquisition of Bosch Chassis Systems India Private Limited for up to ₹9,068.68 crores, enhancing mobility portfolio and automotive safety systems position.

BHEL - Emerged as lowest bidder (L1) for thermal power package worth Rs 10,300 crore. Signed Technology Collaboration Agreement with E2S Company Limited (South Korea) for excitation systems for synchronous machines supporting ‘Make in India’. 💯☑️

Colgate-Palmolive - Launched free dental check-up initiative on World Health Day; 4.5+ million dental screenings since 2024-25, addressing 9 out of 10 Indians dental issues.

Max Healthcare - a=Acquisition of 58.39% stake in Kalinga Hospital Ltd for ₹300 Crore; loan of up to ₹100 Crore for Kalinga Hospital renovation; corporate guarantee for refinancing.

HCL Tech - Announced three acquisitions in December 2025 including Hewlett Packard Enterprise’s Telco Solutions business, strategy to enhance AI and business intelligence capabilities. US subsidiary plans to lay off 120 employees in Orlando Florida from May 29 through December 31, as part of operational restructuring linked to client project rampdown.

Infosys - Made two acquisitions in 2025 to bolster AI execution capabilities, invested over $800 million in FY26 acquisitions. Partnered with Harness for AI-led software delivery transformation leveraging Infosys Topaz and Cobalt. 💯☑️

Bharat Forge - Board approved phased restructuring proposal for German subsidiary BF CDP, may involve wind-down and solvent liquidation; approved financing arrangement up to EUR 30 million.

Cyient - Cyient Semiconductors Singapore acquired 74% stake in Kinetic Technologies for USD 85 million, following December 17, 2025 announcement.

ixigo (Le Travenues Technology - Partnership with Swiggy via ixigo Trains and ConfirmTkt for on-train food delivery from 40,000+ restaurants across 160+ stations with real-time tracking.

Ola Electric (OLAELEC) - Promoter and CMD announced new LFP cell ready for production with thousands of vehicles on road; new cell format to reduce vehicle costs and accelerate EV adoption in Gigafactory scale-up. 💯☑️

TVS Motor - Launched Armado 200 three-wheeler for Indonesia commercial sector with 197.75 cc engine, 840 kg payload, introductory price IDR 34,900,000.

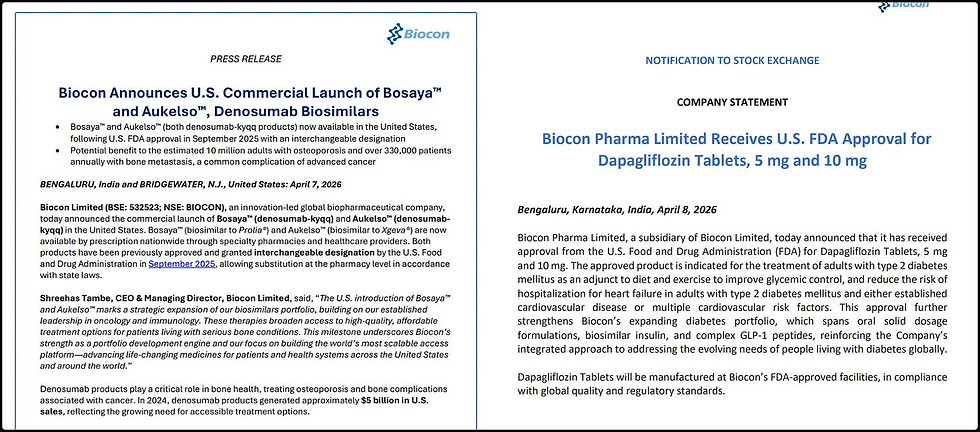

Biocon - Biocon Pharma received USFDA approval for Dapagliflozin Tablets 5 mg and 10 mg for Type 2 diabetes. Intensifying AI focus with advanced data science tools, expected revenue uplift 3-5% with cost savings over 3-4 years, established steering committee. Announced US commercial launch of Bosaya and Aukelso (denosumab biosimilars) following September 2025 FDA approval. Kiran Mazumdar-Shaw called for new IPO rules to support biotechnology innovation. 💯☑️

Tejas Networks - Won Golden Peacock Innovative Product/Service Award 2026 for WavePlexus RAN portfolio recognizing corporate innovation and sustainability.

Jindal Stainless - Appointed Bollywood actor Ranveer Singh as first-ever brand ambassador to enhance brand visibility with multi-platform campaigns highlighting stainless steel’s role in India’s development.

Sona Comstar (SONACOMS) - Produced 500 million differential gears and 10 million differential assemblies, market share increased to 8.7% in 2025 from 4.5% in 2019. 💯☑️

ONGC - Awarded Rs 59 crore contract to Deep Industries for natural gas services. Government considering cap on ONGC new well gas price (currently $12.91/mmbtu vs $8.9 deepwater ceiling) amid distributor concerns. 💯☑️

Titan - Launched coloured gemstone jewellery range ‘Hues’ under Tanishq with 200+ designs targeting younger consumers, priced ₹40,000-2.5 lakh. Modified Titan Employee Stock Option Trust deed due to trustee composition change. 💯☑️

ACME Solar - Successfully commissioned fifth phase of BESS Project adding 76 MW/160.512 MWh, total commissioned 247 MW/521.652 MWh out of planned 285 MW/601.904 MWh.

Nykaa (FSN E-Commerce) - In talks for majority stake in skincare brand 82°E; Kay Beauty JV reported 50% revenue growth to Rs 132.4 crore in FY25. Confirmed ongoing discussions for 82°E acquisition, filed Q4 FY2026 revenue update. Reported Q4 FY2026 GMV growth in late twenties and NSV growth in early thirties, highest in 12 quarters, opened 26 new stores, total 313 as of March 31, 2026. 💯☑️

Nazara - Raised ₹500 crore focusing on global expansion including Spain gaming studio acquisitions, emphasizing social gaming and AI strategies. LVL Zero incubator (Nazara-backed) selected 10 gaming startups for inaugural cohort focusing on PC and console premium gaming. 💯☑️

IRFC - Sanctioned and fully disbursed Rs 1,000 crore term loan to Maharashtra State Power Generation Company (MAHAGENCO), strong start to financial year.

NCC - Awarded Rs 488 crore construction contract by BPTP for residential development in Gurugram, experienced in residential, commercial, and infrastructure.

Bajaj Auto - Experiencing supply chain disruptions from Iran war affecting Tier-2 supplier parts.

Aurobindo Pharma - CuraTeQ Biologics subsidiary reported positive Phase 3 results for Omalizumab biosimilar BP11 in 608 patients, meeting all primary endpoints, supporting regulatory submissions for chronic spontaneous urticaria. Received USFDA approval for Dapagliflozin and Metformin Hydrochloride ER Tablets (US$ 514 million market), launching immediately with 180 days shared exclusivity. Also received USFDA approval for Dapagliflozin Tablets 5 mg and 10 mg bioequivalent to Farxiga ($10.2 billion market).

YES Bank - Vinay M Tonse laid out four-pillar growth blueprint (people, products, processes, technology) as new CEO, shifting from recovery to expansion. Released updated KMP list for materiality determination per SEBI. Announced appointment of Mr. Vinay Muralidhar Tonse as new MD & CEO effective April 6, 2026 following Mr. Prashant Kumar’s tenure completion, Tonse previously at SBI.

OneSource Specialty Pharma - MD & CEO Neeraj Sharma mentioned unexpected delay in Canadian approval for Semaglutide, supply chain diversification intact, capex partly funded by customer payments and debt. Sole supplier of Semaglutide to Dr Reddy, Canadian approval expected by May with risk of inventory build-up. 💯☑️

Fortis - IHH Healthcare aims to hike stake in Fortis to 50%, Fortis showing strong EBITDA margins 23-24%, expanded hospital count from 27 to 36 including Gleneagles

Texmaco Rail (TEXRAIL) - Awarded Rs. 39.26 crores order by Southern Railway for design, supply, erection, testing, commissioning of 25kV Traction Over Head Equipment, 36-month completion.

NMDC - Increased iron ore prices by up to 11.1% effective April 5, 2026, record FY 2025-26 production of 53 million tonnes, sales 50.23 million tonnes (13% increase).

Ethos - Inaugurated new Ethos Watch Boutique in Jodhpur Rajasthan (94th boutique in India). Also opened new Ethos Watch Boutique in Mumbai (93rd boutique in India). 💯☑️

Waaree Energies - Subsidiary Sangam Solar One Private Limited commenced operations at new solar module manufacturing facility in Samakhiali-Kutch Gujarat with 3000 MW annual capacity.

Diamond Power Infrastructure (DIACABS) - Received letter of intent from Adani Power for supply of power and control cables at Raipur Ph-II Thermal Power Projects worth Rs. 43.26 crores by July 31, 2026. Received LOI from Adani Electricity Mumbai for cable supply worth Rs. 100.54 crore (April 2026-February 2027). Received LOI from Adani Green Energy for cable supply worth Rs. 19,57,11,313 within 15 days. 💯☑️

KRN Heat Exchanger - Subsidiary KRN HVAC Products received export order for Heat Exchanger Coils worth INR 55 Crore as part of normal business operations. 💯☑️

WeWork India - Signed five long-term lease agreements adding 700,000+ sq. ft. office space across Bengaluru, Hyderabad, Chennai including 12,000 desks, reinforcing South India flex workspace leadership.

Alembic Pharmaceuticals - Received final USFDA approval for Dapagliflozin Tablets 5 mg and 10 mg for Type 2 diabetes; 180 days shared generic exclusivity, US$ 10,487 million estimated market size.

Torrent Power - CCI approved acquisition of 100% equity in Nabha Power from L&T Power Development for enterprise value Rs 6,889 crore; operational capacity to increase from 5 GW to 6.4 GW.

Newgen Software - Qatar Court of Cassation dismissed appeal against adverse Investment and Trade Court judgement; liable to pay USD 1,370,000 and QAR 200,000 damages;

NLC India - Among 25 companies attending pre-bid conference for Rs 7,280-crore rare earth permanent magnet scheme.

Apollo Tyres - Focusing on growth strategy including empowering women drivers, EV adoption, global uncertainties; double-digit India growth despite Europe challenges.

Indian Hotels (INDHOTEL) - IHCL expanded portfolio to 628 hotels (373 operational, 255 pipeline, record 250 signings this fiscal year.

Lemon Tree Hotels - Received CCI approval for acquisition of equity shares of Fleur Hotels by Coastal Cedar Investments BV and internal restructuring via amalgamation and demerger.

PVR Inox - Introducing new cinema experience eliminating traditional ticketing, focusing on gourmet movie experiences.

CarTrade Tech - OLX India appointed Varun Sanghi as Non-Executive Chairman to guide OLX India’s growth phase with innovation and customer-centricity focus.

Titagarh Rail Systems - Subsidiary Titagarh Naval Systems received in-principle approval from Directorate General of Shipping for Rs 610 crore expansion project enhancing shipbuilding infrastructure.

Smartworks - Expanded multi-city managed office deal with Forbes 2000 global CX leader; client portfolio now over 5,000 seats across four cities; expected rental revenue from these locations projected to exceed INR 155 Cr.

EPL - Announced merger with Indovida India Pvt Ltd at 70% premium creating combined entity valued at $2 billion, aims to enhance position in consumer packaging market particularly emerging markets.

Visual Artifact (Must View)

If you are lazy or do not want to read filings, which many of you will not, then this is for you. An easy way to read everything from macro to micro stuff in one place.

And anything shared here in artifact is not a buy or sell recommendation. This is just a visual representation for viewers to understand the market outlook better. So this is only for studying purpose. Take inspiration from this, but do not follow it if it gives any holding recommendation

This is very short, but you will get it if you read line by line :)

India market pulse Part 1 - https://claude.ai/public/artifacts/42d8a960-9790-4bbb-b65c-cdb1df06e59c

India Market Map Macro Part 2 - https://claude.ai/public/artifacts/2e877770-80e9-4a59-9763-bd846b434f88

What I like this Week in Filings (Must Read 💯☑️)

EIEL order book is ₹30,926 million (water/wastewater ₹28,365 million; renewables ₹2,561 million) with a bid pipeline of ₹5,000 crore. They also secured five projects worth ₹1,481 crore in March 2026, including ₹1,070 crore in BESS orders. That BESS entry is the real story they’re quietly building, they’re no longer just a sewage EPC, they’re becoming a multi-vertical infrastructure player (water + wastewater + ZLD/CETP + battery storage + renewables).

24 months completion is aggressive for sewer networks spread across 306 ULBs. Execution across that many sites simultaneously is a logistics nightmare.

Syrma SGS is constructing a new PCB manufacturing facility in Naidupeta Industrial Zone, Andhra Pradesh through this JV - single-layer and multi-layer PCBs, joint venture with Shinhyup Electronics. The JV is a ₹1,595-1,600 crore PCB/CCL/EMS project on 26.7 acres with groundwork already started. It manufactures multi-layer Printed Circuit Boards and Copper Clad Laminates.

But Syrma has been on a different acquisition spree parallel to this. They’re acquiring 60% of Elcome Integrated Systems (defence + maritime electronics) for ₹235 crore, with remaining 40% on earn-outs tied to FY26/27/28 milestones. And a separate JV with Elemaster Group (European) for railway/industrial/medical high-reliability electronics in Bengaluru. Plus a separate JV with Premier Energies for solar inverters.

So the Shinhyup name change filing is a single tile in a much bigger mosaic - Syrma is deliberately building out: (a) PCB capacity via Shinhyup JV, (b) defence electronics via Elcome, (c) European OEM exposure via Elemaster, (d) renewable electronics via Premier Energies.

Syrma is building the only Indian company positioned across PCB + defence electronics + railway/industrial + solar inverters simultaneously. Much higher beta to India’s electronics story than Kaynes or Dixon individually. if it work out, this is watch out Player, they are doing very serious Integration, even I told yu in blue Economy Article in which Syrma have good skin in the Game.

Graphic Films - adhesive-backed films for hoardings, window graphics, vehicle wraps, retail branding surfaces. Entering a category traditionally dominated by PVC-based materials. This is a commodity-adjacent market but volume-large. Every mall signage, every metro station ad, every retail window display uses these. Garware’s polyester chip-to-film integration gives them raw-material advantage over PVC converters.

Cloaking Films - specialized privacy films for glass surfaces that enable clear visibility through glass while restricting visibility of digital screens. This is a niche but premium use case, think conference rooms where someone outside can see people inside but can’t read laptop screens through the glass. High ASP, low volume, differentiated.

PDLC Smart Films - intelligent glass film that switches between opaque and transparent states with electricity - privacy on demand for conference rooms, modern offices, adaptive architectural spaces. This is the one that matters most. PDLC (Polymer Dispersed Liquid Crystal) smart films are a high-growth architectural category globally - premium offices, luxury homes, hospital ICUs, hotels all installing switchable glass.

Garware making this at scale in India replaces imports and enters a category with structural tailwinds (smart offices, green buildings, commercial real estate premiumisation).

Paint Protection Film was their first specialty win (grew from 5% of mix to 30%+). Smart Films could be the next 5-year leg. The TAM for smart films + cloaking + graphic films in India is arguably bigger than PPF because it taps into real estate + advertising simultaneously, both structural growth stories. If new product ramp adds 200-300 bps to blended margin in FY27, the stock re-rates.

Organon is Merck 2021 spinoff holding women’s health (contraception, fertility, Nexplanon), biosimilars, and established branded generics. Revenue $6.2bn in 2025. But it’s trading at $1.8bn market cap because debt is $8bn and sales are flat-lining. Sun is essentially buying a $6bn revenue pharma company for a 2x sales price for a branded/innovative portfolio.

For Sun, which is overweight on generics and specialty (Ilumya, Odomzo), this instantly plugs a branded-products hole in the US and gives them a global women’s health franchise where competition is thin. Sun has $3.2bn net cash, so they’d lever up maybe $9bn, doable if margins hold.

Why it could be Ranbaxy 2.0 - Sun bought Ranbaxy in 2014 for $4bn and spent the next 5 years cleaning up USFDA issues, Halol/Mohali plant problems, and inherited litigation. It nearly broke the company growth trajectory. Organon has its own baggage, declining US sales, goodwill impairment in Q4 2025, and that $8bn debt doesn’t magically vanish.

Integrating a US-listed entity with commercial ops across 90+ countries is a different animal than consolidating a domestic peer. And paying premium for a business whose top-line is shrinking means Sun needs a turnaround synergies.

Dilip Shanghvi is making the biggest bet of his career at age 70. He sees Organon portfolio as undervalued + Sun balance sheet strength as a once-in-a-decade arbitrage.

If the binding offer goes through, Sun becomes a branded-pharma + women’s health global player with US front-end ownership. This is a high-conviction binary event.

This is the first SPV under the January 2024 MoU with PEAK to build 100 Bio-CNG plants across India, GCC, Africa and Europe. Ghaziabad is plant #1 going formal. This is a pilot-to-scale play.

Most CBG plays in India are agri-residue based (straw, cattle dung) - unreliable feedstock, seasonal, logistics-heavy. Wabag is doing something different - STP-linked CBG, meaning they’re converting sewage treatment plants into bio-gas production centres.

Feedstock is sewage sludge - guaranteed, year-round, urban, already aggregated at the STP. Wabag operates 40+ biogas generation facilities globally and produces 40+ MWh of green energy today. This isn’t greenfield risk, it’s monetising existing infrastructure.

Wabag is building an energy transition services company inside a water company. PV-linked desalination, green hydrogen water, semiconductor ultra-pure water (UPW), bio-CNG, AI-driven plant operations. Every one of these is higher-margin, technology-led, and energy-transition-aligned. Water is becoming infrastructure, water + energy is becoming strategy.

When a company moves from MoU to SHA, you’re looking at 12-18 months to commissioning. Ghaziabad plant commissions → rev recognition → template for 99 more plants. If even 30 of the 100 plants scale in 3-4 years, Wabag becomes a meaningful CBG player alongside IOC, BPCL, HPCL’s own bio-gas programmes.

Stop thinking of Wabag as a water stock. Think of it as a technology-led industrial services platform with water as the anchor product. trades at a big discount to global water peers (Veolia, Xylem trade at 28-35x). The Ghaziabad SPV is Step 1 of 100, track how fast Step 2, 3, 4 come. That cadence is the stock catalyst.

Datamatics has been a sleepy BPO services company for decades This filing is their attempt to break out of that zone. TruAI Underwriting isn’t just a product launch, it’s the first product in what they’re calling their TruAI enterprise suite. TruAI Underwriting is the first solution in this portfolio, which means more verticals are coming (claims, onboarding, KYC, fraud).

Why underwriting specifically? Because it’s the most painful, judgement-heavy, document-intensive process in insurance and Datamatics already processes this manually for global insurers as a BPO. A leading life insurer in India was processing more than 40,000 applications per month in their case study, and Datamatics cut TAT to 40 seconds per application. They’re essentially productising their own BPO workflow into an AI SaaS product and selling it back to the same clients at platform margins instead of per-seat margins.

This is the exact same playbook Coforge, Infosys, TCS, Persistent are running. Every Indian IT/BPO company is racing to repackage services as AI products. The question is whether Datamatics can compete when Coforge has 130+ pre-built agents and Infosys has Topaz Fabric. Datamatics edge is depth in insurance BPO - they’ve seen every form, every lab report, every exception case. That’s a moat, but it’s narrow & Niche.

You have to understand the hotel tech stack to get why this matters. A hotel uses a PMS (property management system - Hotelogix is one) to run daily ops. Separately, they use a channel manager to push rates to OTAs (Booking, MakeMyTrip). Separately, they connect to GDS (Amadeus, Sabre, Travelport) to reach corporate travel agents. Each integration is a different vendor, different contract, different fees. This is exactly the fragmentation hell that independent hotels complain about.

RateGain UNO Platform is trying to become the one integration layer that sits inside the PMS and handles all downstream distribution. The collaboration enables Hotelogix’s 12,000+ hotel customers worldwide to access major distribution networks including Amadeus, Sabre, and Travelport, reaching over 600,000 travel agents and corporate programs directly within their existing PMS environment.So instead of 12,000 hotels each signing separate deals with Amadeus + Sabre + Travelport, they get it bundled through their existing PMS and RateGain collects the toll on every booking flowing through.

This is the third such platform partnership in 2 weeks - RateGain Partners with Razorpay as Platinum Partner for RG Pay (April 2) and RateGain Partners with Cashfree Payments as Platinum Partner for RG Pay (March 26). RateGain is aggressively stacking partnerships to make UNO the default middleware for hotel distribution and payments. The strategy is classic platform play lock in the PMS providers (Hotelogix, etc.) and you automatically lock in every hotel they serve.

The revenue impact of any single partnership is small - Hotelogix is mid-market, not Marriott or Hilton. But the direction is right. RateGain already serves 13,000+ customers and 700+ partners across 160+ countries. Each partnership adds incremental GDS transaction volume, and GDS is a higher-margin product than channel management.

UNO is becoming real infrastructure, not a feature. The economics here are SaaS + transaction fee - both scale with network effects, If they cross 5-6 PMS integrations in 2026, UNO becomes genuinely moated.

HBL Engineering Shares Drop 14% After Missing Major Kavach Locomotive Tender Jan 16, 2026. So they don’t win everything. The market punished them hard on that miss. The current stream of PLW + BLW + ICF orders is essentially the market reclaiming the monopoly narrative that was briefly dented.

Order book on KAVACH alone was ₹3,763.83 crore and is now well north of ₹4,500 cr with these fresh additions. Against FY26 run-rate revenue of roughly ₹3,500-4,000 cr, that’s 1.2x book-to-bill on KAVACH alone.

Individually, an ₹83 cr order from a small-ish loco works isn’t moving the needle. Collectively, HBL is becoming the sole branded supplier of KAVACH 4.0 to Indian Railways, and this market is going to ₹40,000+ cr over 5-7 years as 44,000 route km gets deployed. Until a second Ver 4.0 RDSO approval comes through, HBL keeps eating.

Launched AI Mod Squads (subscription-based human+agent delivery model). Announced $2.5 billion revenue target by FY27 from AI-native engineering.

First, the $2.5 billion FY27, It’s from the $2.35 billion Encora acquisition announced December 26, 2025 - the largest ever ER&D acquisition by an Indian IT company. Post-acquisition, the combined entity is expected to have annual revenues of $2.5 billion, with AI-led engineering, data and cloud services alone likely to deliver $2 billion revenue in FY27. So Coforge today = $1.9B combined run-rate with Encora, growing to $2.5B by FY27.

Second - AI Mod Squads is how they plan to monetise this.Think of it this way - traditional IT services = ₹X per hour per engineer, linear scaling. AI Mod Squads = fixed monthly subscription for a squad of (say) 3 AI agents + 2 senior engineers that deliver a specific outcome. By moving from effort based pricing to a transparent outcome focused subscription model, we are giving clients cost predictability while enabling acceleration of our customers’ transition to autonomous AI driven enterprises.

This is a fundamental shift from T&M (time & materials) to SaaS-like pricing. A banking loan origination human-agent squad has generated a 70% reduction in cycle time, and an insurance underwriting human-agent squad has led to a 50% faster underwriting cycle.

Why this matters for valuation - T&M revenue gets valued at IT services multiples (18-25x PE). Subscription-based AI product revenue gets valued at SaaS multiples (40-60x PE). If Coforge can prove even 20-25% of revenue on the subscription model, the re-rating potential is significant. The risk: customers have to actually pay for outcomes instead of hours, and procurement teams in banks/insurers are hardwired to buy FTEs. Adoption curve will be slow.

Coforge saying - we’re not just acquiring AI capability - we’re productising it and changing the pricing model. The ₹1,815 preferential allotment to Encora PE shareholders means 21% dilution is coming. So EPS math is FY27 EPS accretive but only marginally. The real call is whether subscription model pricing catches on.

Pay attention to Infosys acquisition spend in FY26 has reached $808 million, surpassing that of its peers, including Tata Consultancy Services (TCS), HCL Technologies, and Wipro. TCS has spent $773 million on acquisitions in the current fiscal, while HCLTech and Wipro have spent $400 million and $375 million, respectively.

Infosys is the most acquisitive large-cap Indian IT company in FY26, which is a significant behavioural change from the Narayana Murthy / Vishal Sikka era where Infosys was famously M&A-cautious.

The two deals - Infosys Limited announced it will acquire Optimum Healthcare IT for up to $465M (US healthcare IT consultancy) + Stratus Global (also referred to as Stratus), an insurance technology solutions provider, for $95 million. Both are vertical-specific - healthcare and insurance, exactly the two highest-margin regulated verticals where AI has the most to disrupt. 2,000 new employees expected to be added, including 1,600 from Optimum Healthcare and 450 from Stratus.

Compare the strategy to Coforge. Coforge bought one big thing (Encora) in an all-stock deal and is productising. Infosys is doing string-of-pearls - many smaller, vertical-deep acquisitions paid in cash. Different philosophies - Coforge wants horizontal platform scale, Infosys wants vertical depth + immediate revenue accretion. Infosys approach is lower-risk (each deal integrates fast, smaller disruption)

Infosys is making a defensive aggressive play - aggressive on capital deployment, defensive in that it’s buying what it can’t build fast enough. The Harness deal signals Infosys knows the AI-native services era is here.

Promoter and CMD announced new LFP cell ready for production with thousands of vehicles on road; new cell format to reduce costs and accelerate EV adoption in Gigafactory scale-up.

New 46100 cylindrical format to enter products from next quarter. Red flag - zero specs disclosed. No energy density (Wh/kg), no cycle life, no charge rate, no BIS/ARAI certification, no third-party test results. In an industry where CATL and BYD routinely publish detailed specifications when announcing new cells, Ola will also have to publish the same sooner than later. Energy density is the single most important battery metric. Wait for it :)

if Ola genuinely has a working 46100 LFP cell going into vehicles in Q2 FY27, even at mediocre yield and modest energy density, it structurally changes their cost base. LFP batteries are safer, last longer, and cost less than current NMC cells, a move expected to significantly lower EV prices and boost adoption in India. Battery is 30-40% of an e-scooter’s BOM. In-house LFP cell at even 80% of benchmark efficiency could cut scooter cost by 10-15%. That’s the upside case.

USFDA approval for Dapagliflozin 5mg and 10mg for Type 2 diabetes. US commercial launch of Bosaya and Aukelso (denosumab biosimilars to Prolia and Xgeva). AI steering committee set up, 3-5% revenue uplift expected over 3-4 years.

Biosimilars as a category have become commodity generics with better branding. The right question is not did they get approvals but are they first, second, or sixth to market and on both these launches, they’re late. For a biosimilar thesis, you want the company launching BEFORE the crowd (Alvotech model), not with it. Until the GLP-1 biosimilar pipeline (semaglutide, tirzepatide) enters the conversation with differentiated timing, Biocon is a revenue-grower, not a margin-grower.

This is not a collection launch, it is a category bet. Tanishq is formally entering natural coloured gemstone jewellery in India - a fragmented, trust-deficit, largely unorganised category where Indian consumers are worried about buying gemstones because they don’t know the origin or whether the price they are paying is right.

Tanishq’s standard organised-sector moat - transparent pricing, lifetime maintenance, and 100% exchange value - maps perfectly onto this trust gap, the same way they formalised diamond jewellery two decades ago. If they execute, they don’t just sell Hues, they become the default buyer for every emerald, tanzanite, and tourmaline purchase in urban India over the next five years.

The strategy is the 18kt (not 22kt) gold choice. 22kt is investment gold - heavy, traditional, bought at weddings. 18kt is design gold - lighter, lower gold content, higher making charges as a percentage of ticket.

This means: (a) lower gold-price sensitivity per piece, so demand is less volatile when gold runs up or corrects; (b) higher gross margins because making charges are pure operating leverage (c) aligns with the target consumer - a younger, everyday-wear buyer who values design over gold weight.

Triptii Dimri as face + express yourself positioning + ₹30k entry price = they are deliberately pulling the category down into millennial/Gen Z discretionary-spend territory, away from the occasion-only, mother-of-the-bride frame. This is the exact same thinning-out-of-gold-content strategy that global jewellers (Cartier, Bulgari) have ridden to premium margins.

Jewellery business has been under pressure from lab-grown diamond cannibalisation and gold price volatility - Hues gives them a third growth leg that sidesteps both problems. Coloured gemstone as a category is estimated at ₹15,000-20,000 cr in India and 90%+ unorganised - exactly the Tanishq sweet spot.

In talks for majority stake in skincare brand 82°E (Deepika Padukone’s). Kay Beauty JV revenue grew 50% to ₹132.4 cr in FY25. Q4 FY26 GMV growth in late twenties, NSV growth in early thirties, highest in 12 quarters. Added 26 stores, total 313.

Strip the celebrity narrative and 82°E looks distressed. The brand reported a 30% year-on-year decline in revenue to Rs 14.7 crore in FY25 and a loss of Rs 12.26 crore, last valued at roughly ₹90 cr. Launched in 2022, priced at around ₹2,500 for 50 ml products, positioned as premium clean skincare and it didn’t work, because Minimalist, Dr Sheth’s, Foxtale and a wave of digital-first brands out-marketed and out-distributed a celebrity D2C that never figured out scale.

Nykaa is not acquiring growth, they are acquiring a struggling brand that happens to carry the biggest female celebrity endorsement in Indian cinema. The pitch inside Nykaa is obvious, we have 42 million beauty customers, we can put 82°E on the front page, cross-sell it via our store network, and rehab the brand within 18 months but turnarounds in beauty are hard. Wait and Watch Guys :)

Ignore the headline M&A and look at Q4. NSV growth in early 30s with 313 stores is the story - Nykaa has broken out of its post-IPO compression. For the stock, operating leverage finally kicks in from here. 82°E is small enough that even if the turnaround fails, it’s a rounding error on Nykaa P&L, if it works, it adds brand equity and gives Deepika skin in the game as a quasi-shareholder.

KRN makes aluminium and copper fin-and-tube heat exchanger coils - the critical thermal component in every air conditioner, chiller, condenser, and data-centre cooling system. As hyperscaler and colo data-centre buildout accelerates globally (US, Europe, Canada, UAE are their export markets), demand for high-quality fin-tube coils is structurally short.

India has been a cost-advantaged supplier of these coils because of cheap aluminium extrusion and tube-manufacturing economics, and KRN is the largest pure-play listed name in the space. They are essentially the TD Power Systems of the HVAC value chain - a niche component feeding into a massive end-market tailwind they don’t have to market themselves. The subsidiary structure (KRN HVAC Products) suggests they are ring-fencing the exports book.

One caution - part of normal business operations is the giveaway line. This is not a one-off trophy order, it is embedded demand, so the next leg depends on margin expansion from backward integration (in-house tube manufacturing) and data-centre order-book concentration rising as a percentage of total revenue.

This is the kind of filing where the number matters less than the cadence. ₹55 cr order on its own is 12% of FY25 revenue, meaningful but not earth-shaking. The data-centre cooling angle is the unlock - every 100 MW of new data-centre capacity requires ₹40-60 cr of HVAC coil content, and India alone will add 2-3 GW of DC capacity by FY28. KRN is a pick-and-shovel play on data-centre capex, consumer AC growth, and cold-chain expansion simultaneously.

My Biased Opinion On This Week Filings :)

Nothing big came this week in the market, but some of the interesting filings I read today are really, really good.

Syrma SGS - you have to read about this company. They are going into different segments of electronics, from PCB to naval defence to IoT things.

Garware Hi-Tech - they are in the valued segment, & they are launching new products. This is the second time they are launching new products, so I feel the time is ripe. Even the company, due to tariff, has gone down but they will do good.

Datamatics - if you read their improvement from AI integration, and if you link it with Coforge or other info, or even Infosys also, in the combination of things, you will find IT is going in the SaaS direction and subscription-based, and somewhat in that segment. What you have to look at is the balance - Datamatics balance sheet is really, really good. But when you compare with Coforge, you don’t know what lies ahead and how this will go on. That you have to link wih it, what if Coforge enter into Datamatics business.

RateGain is going good. If you look at that company - it is distribution-led, AI-led, integration-led, and supply chain-led business. With the travel ecosystem, the whole supply side is in the hand of RateGain. So in the next 5 years, the company will do really, really better, monopolistic in nature in some way

Nykaa - as a platform business, is now improving from what they have done at the IPO level, their portfolio level, and their NAV. Their metrics are really better than the past, and with distribution-led store growth, I think in the next 3 to 5 years the company will do much better than what they are doing today, because of the Indian economy. If you correlate with the Indian personal care and cosmetic industry.

KRN Heat Exchanger as I told you in the past, they will be some level of proxy to a data centre. They are getting orders from the international market for the things they make. Even in the last Q3 they said they will be more focused on export - they want 50% to come from export, so they are going in that direction. That is how you can see whatever they are doing- they are getting orders, and they are even forming a subsidiary.

Reading these filings, I found three companies really good this week:

RateGain - if you read it, RateGain will be a monopoly in some way. If this goes the right way, then good.

VA Tech Wabag - if you are in water treatment management service, they have their energy proxy to bio-gas, and the level they will produce will be interesting to watch out how it will pan out. If you read it, they will even be in the future semiconductor and data centre water recycling. If you look at the long-term perspective of Wabag, Wabag will be much better than any other water/wastewater/recycling system player. This is the one player I like the most.

Garware Hi-Tech - will do well because of the newly launched new product, the increasing product-launching scope, and the valued segment that has helped the margin level. I feel even with the trade tariff, with their Dubai subsidiary newly formed - this company will do better from here :)

My View on Market

Market is already at the bottom, and whatever the worst-case scenario was, it’s already past. Whatever has happened, has happened. Ransomware hack, gas crisis, drone attack - whatever is happening, Middle East will continue to be unstable in the future too.

If you look at now, the negotiation is happening - Trump Iran, and Pakistan is the broker, or whatever is happening. That will continue. You have to live with it. This is going to continue. For the utility with the state, there is an election in November in the US, so this will continue and you have to make a discount on that accordingly.

The Indian government is doing whatever is possible, whatever they can do, they are doing it. It’s not like they are not doing anything. We are looking at minerals exploration, and this will be the big factor in the current decade for refining these energy plays. This way, data centre, AI, and infrastructure play in manufacturing will stay. We have to look at the sectoral tailwind sector, okay.

The most important one is that volatility will continue. That will stay in the market. We have to live with it. It will go up and down as of now, but the most severe phase is gone. This is slowly ramping off, and in FY27 Q1 or Q2 we will slightly see things changing.

You have to see the productivity data, nominal GDP data, and other reflecting data and industry data to see how things will change and most importantly, the quarterly result. That is the most important - how things are going on. For me, that is really, really important.

Now the stock picking and searching time is going out. This is the last phase. After this, you will not find stocks at the right value - even most of them are already out of the zone where you can buy them. Whatever discount is there will soon be gone.

As of now, I am bullish on India and I am positive. My cash level is just 3%. I don’t know if I will keep it but I keep it for emergency or whatever. Whenever I feel right, I will deploy it.

BONUS

Read these Articles :)

Wow, Interesting